Sako Kady, Mpinda Berthine Nyunga, Rodrigues Paulo Canas

African Institute for Mathematical Sciences (AIMS)-Cameroon, Limbe P.O. Box 608, Cameroon.

Department of Statistics, Federal Universityof Bahia Salvador, Salvador 40170-110, Brazil.

Entropy (Basel). 2022 May 7;24(5):657. doi: 10.3390/e24050657.

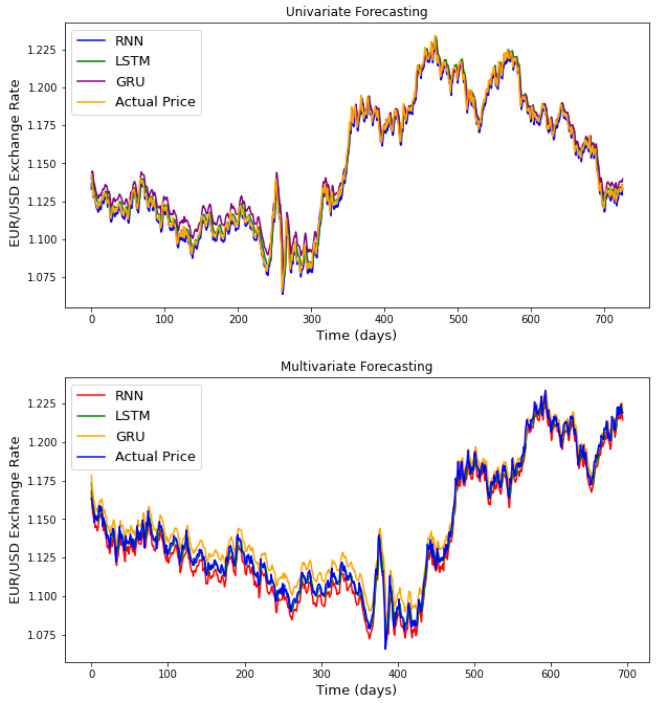

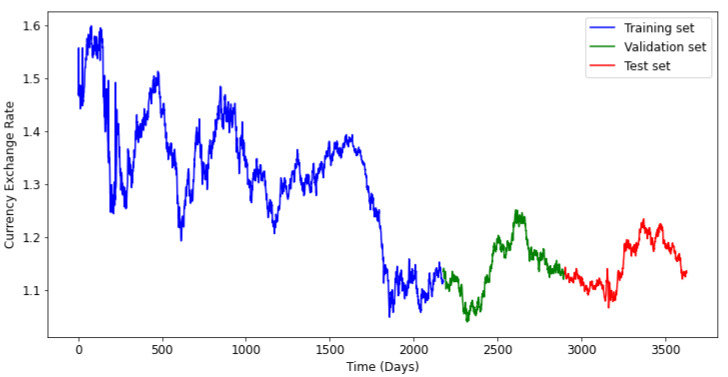

Financial and economic time series forecasting has never been an easy task due to its sensibility to political, economic and social factors. For this reason, people who invest in financial markets and currency exchange are usually looking for robust models that can ensure them to maximize their profile and minimize their losses as much as possible. Fortunately, recently, various studies have speculated that a special type of Artificial Neural Networks (ANNs) called Recurrent Neural Networks (RNNs) could improve the predictive accuracy of the behavior of the financial data over time. This paper aims to forecast: (i) the closing price of eight stock market indexes; and (ii) the closing price of six currency exchange rates related to the USD, using the RNNs model and its variants: the Long Short-Term Memory (LSTM) and the Gated Recurrent Unit (GRU). The results show that the GRU gives the overall best results, especially for the univariate out-of-sample forecasting for the currency exchange rates and multivariate out-of-sample forecasting for the stock market indexes.

金融和经济时间序列预测从来都不是一项容易的任务,因为它对政治、经济和社会因素很敏感。因此,投资金融市场和货币兑换的人通常在寻找强大的模型,以确保他们尽可能最大化收益并最小化损失。幸运的是,最近各种研究推测,一种称为递归神经网络(RNN)的特殊类型的人工神经网络(ANN)可以提高金融数据随时间变化行为的预测准确性。本文旨在使用RNN模型及其变体:长短期记忆(LSTM)和门控循环单元(GRU)来预测:(i)八个股票市场指数的收盘价;以及(ii)与美元相关的六种货币汇率的收盘价。结果表明,GRU给出了总体最佳结果,特别是对于货币汇率的单变量样本外预测和股票市场指数的多变量样本外预测。